Payday loans are short-term loans. They help you when you need money fast. Many people use them. But they can be costly. The interest rates on payday loans are high. You should know how they work.

Credit: www.incharge.org

Understanding Payday Loans

A payday loan is a small loan. You borrow it until your next paycheck. It is usually for a few weeks. The loan amount is small. It can be from $100 to $1,000. You must repay it quickly.

How Payday Loans Work

You apply for a payday loan. The lender checks your income. They want to see if you can repay the loan. If approved, you get the money. You must repay it with your next paycheck. The lender will also charge you interest and fees.

Interest Rates on Payday Loans

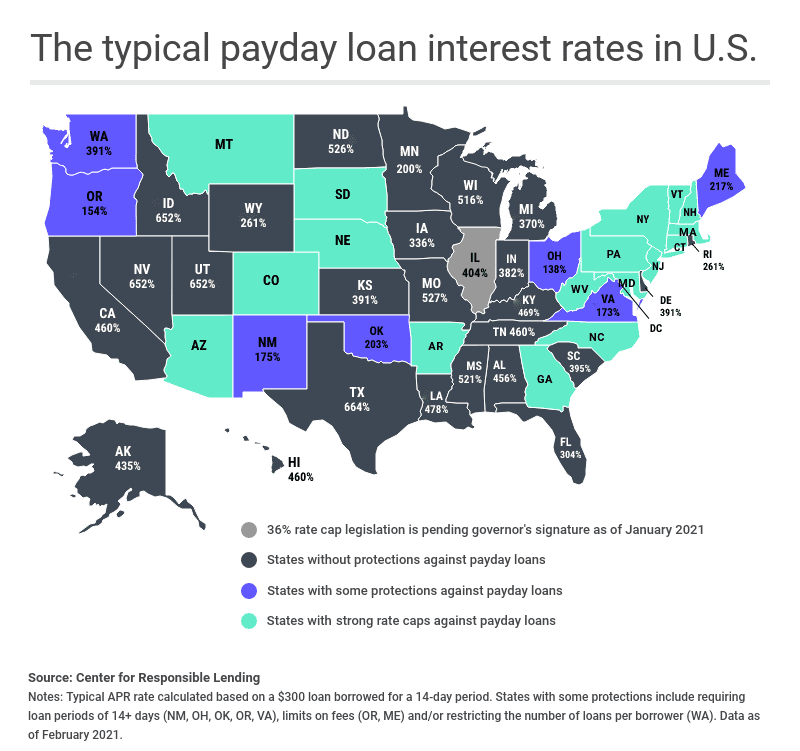

The interest rate on payday loans is very high. It is usually much higher than other loans. The interest rate can be from 300% to 500% APR (Annual Percentage Rate).

Understanding Apr

APR stands for Annual Percentage Rate. It shows the cost of the loan for one year. Payday loans are short-term. But lenders show the interest as APR. This makes it easier to compare with other loans.

For example, if you borrow $100, you might pay $15 in interest. This seems small. But if you calculate it for one year, the APR is very high. This is why payday loans are costly.

Credit: www.sltrib.com

Examples of Payday Loan Costs

| Loan Amount | Interest Rate (APR) | Repayment Amount | Repayment Time |

|---|---|---|---|

| $100 | 400% | $115 | 2 weeks |

| $200 | 400% | $230 | 2 weeks |

| $500 | 400% | $575 | 2 weeks |

As you can see, the cost is high. You repay more than you borrowed. The short repayment time makes it hard. You must be ready to pay back quickly.

Why Are Payday Loan Interest Rates So High?

Payday loans have high interest rates for a few reasons:

- Short term: The loan is for a short time. Lenders charge more for quick loans.

- Risk: Lenders take a risk. Borrowers might not repay. To cover this risk, lenders charge high interest.

- No credit check: Many payday lenders do not check credit. This is risky for them. They charge more to cover this risk.

Alternatives to Payday Loans

Before you take a payday loan, think about other options. There are other ways to get money:

Personal Loans

You can get a personal loan from a bank. The interest rate is lower. The repayment time is longer. This makes it easier to repay.

Credit Cards

If you have a credit card, use it. The interest rate is lower than payday loans. You can repay it over time.

Borrow From Family Or Friends

Ask your family or friends for help. They might lend you money with no interest. This is a good way to avoid high costs.

Local Assistance Programs

Many communities have programs to help. They can give you a small loan or help with bills. Check with local agencies.

Tips to Manage Payday Loans

If you must take a payday loan, be careful. Here are some tips:

- Borrow only what you need. Do not take more than you can repay.

- Understand the terms. Know the interest rate and fees.

- Repay on time. Avoid late fees and extra charges.

- Plan your budget. Make sure you can repay the loan and still cover your bills.

Frequently Asked Questions

What Is A Typical Payday Loan Interest Rate?

A typical payday loan interest rate ranges from 300% to 500% APR.

Why Are Payday Loan Rates So High?

Payday loan rates are high due to short terms and high risk.

How Do Lenders Calculate Payday Loan Interest?

Lenders calculate payday loan interest based on loan amount and repayment period.

Can Payday Loan Interest Rates Change?

Yes, payday loan interest rates can change based on state laws.

Conclusion

Payday loans can help in an emergency. But they are costly. The interest rates are high. It is important to understand the cost. Look at other options first. If you must take a payday loan, be careful. Borrow only what you need. Repay it on time. Plan your budget. This will help you avoid more debt.