:max_bytes(150000):strip_icc()/Pay-Day-Loan-Personal-Loan-dfdeaa22f6ea4790b1c966fcd6c937cf.jpg)

Credit: www.investopedia.com

What Are Payday Loans?

Payday loans are short-term loans. People usually borrow them until their next paycheck. These loans help with urgent money needs. But they can be very costly.

Why Compare Interest Rates?

Interest rates show how much extra money you pay for the loan. Higher rates mean more money to pay back. It’s important to compare rates. This helps you find the best deal.

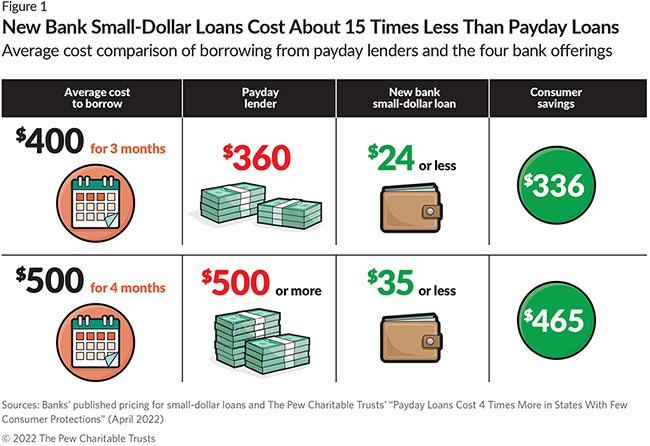

Credit: www.pewtrusts.org

Understanding Interest Rates

Interest rates are the cost of borrowing money. They are shown as a percentage. For payday loans, this rate can be very high. It is often much higher than other types of loans.

How Are Interest Rates Calculated?

Payday loan interest rates are usually calculated in a simple way. You borrow a set amount of money. The lender adds a fee based on a percentage of the loan. You pay back the loan plus this fee.

| Loan Amount | Interest Rate | Fee | Total Repayment |

|---|---|---|---|

| $100 | 15% | $15 | $115 |

| $200 | 15% | $30 | $230 |

Comparing Different Lenders

Not all payday lenders are the same. Each one can have different rates. Let’s look at some examples.

| Lender | Interest Rate | Loan Term |

|---|---|---|

| Fast Cash | 10% | 14 days |

| Quick Money | 15% | 14 days |

| Easy Loans | 20% | 14 days |

Annual Percentage Rate (APR)

APR stands for Annual Percentage Rate. It shows the yearly cost of the loan. Payday loans have very high APRs. This is because they are short-term loans. A 15% interest rate for two weeks can be over 300% APR.

Other Costs to Consider

Interest rates are not the only cost. Some lenders charge additional fees. These can include application fees or late fees. Always check for these extra costs before borrowing.

Impact of High Interest Rates

High interest rates can make it hard to repay loans. This can lead to more borrowing. It can become a cycle. Borrowers can end up paying much more than they borrowed.

Alternatives to Payday Loans

There are other ways to get money. Some options are:

- Borrowing from friends or family

- Using a credit card

- Getting a personal loan from a bank

Frequently Asked Questions

What Are Payday Loan Interest Rates?

Payday loan interest rates are the fees you pay for borrowing short-term money.

How Do Payday Loan Interest Rates Compare?

They are usually much higher than other loan types, like personal loans.

Why Are Payday Loan Interest Rates So High?

Lenders charge high rates because of the short-term nature and high risk of default.

Can Payday Loan Interest Rates Vary?

Yes, rates can vary between lenders and depending on your credit score.

Conclusion

Comparing payday loan interest rates is very important. It helps you find the best deal. Always consider the total cost. Look for other options if possible. Make smart choices to avoid debt.