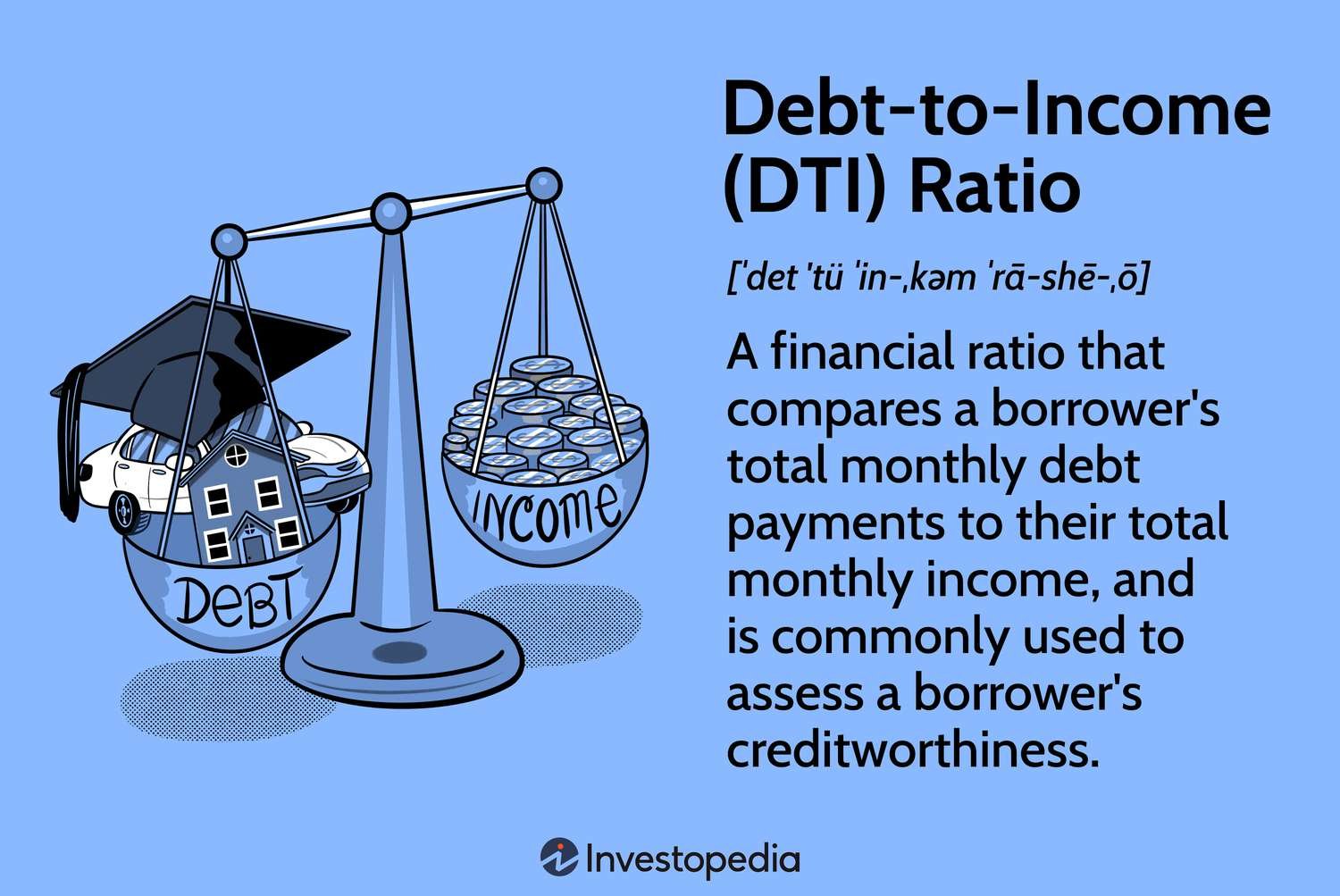

When you want a loan, banks look at your finances. One important thing they check is your Debt-To-Income (DTI) ratio. This number shows how much of your money goes to debt. A lower DTI ratio means you are more likely to get a loan. Let’s learn more about it.

What is Debt-To-Income Ratio?

The Debt-To-Income ratio compares your debt to your income. It is a simple number. It shows how much of your income goes to paying debts. This number helps banks see if you can handle more debt.

How To Calculate Debt-to-income Ratio

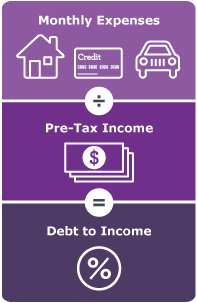

Calculating your DTI ratio is easy. You need two numbers: your monthly debt payments and your monthly income. Here is the formula:

DTI Ratio = (Total Monthly Debt Payments / Gross Monthly Income) x 100

For example, if you pay $500 each month for debt and make $2,000 each month, your DTI ratio is:

DTI Ratio = ($500 / $2,000) x 100 = 25%

This means 25% of your income goes to paying debt.

Credit: www.wellsfargo.com

Why is Debt-To-Income Ratio Important?

Banks use the DTI ratio to decide if you can get a loan. A high DTI ratio means you have a lot of debt. This could mean you might have trouble paying back a new loan. A low DTI ratio means you have less debt. This makes you a better loan candidate.

What Is A Good Debt-to-income Ratio?

Most banks like a DTI ratio below 36%. This means less than 36% of your income goes to debt. A DTI ratio above 43% is usually too high. This makes it hard to get a loan. Different banks have different rules, but these numbers are common.

| DTI Ratio | Loan Eligibility |

|---|---|

| Below 36% | Good |

| 36% – 43% | Fair |

| Above 43% | Poor |

How to Improve Your Debt-To-Income Ratio

If your DTI ratio is high, do not worry. You can improve it. Here are some simple steps:

- Pay down debt: Focus on paying off your debts. This will lower your monthly payments.

- Increase income: Look for ways to make more money. This could be a second job or a raise at work.

- Do not take on new debt: Avoid new loans or credit cards. This will keep your debt from growing.

These steps will help you lower your DTI ratio. Over time, you will be a better candidate for loans.

Real-life Example

Let’s look at a real-life example. Sarah wants a home loan. She makes $3,000 each month. She pays $600 each month for debt. Her DTI ratio is:

DTI Ratio = ($600 / $3,000) x 100 = 20%

This is a good DTI ratio. Sarah has a good chance of getting the loan. Now, let’s say Sarah also has a car loan. She pays $300 each month for the car. Her new DTI ratio is:

DTI Ratio = ($600 + $300) / $3,000 x 100 = 30%

This is still a good DTI ratio. But if Sarah takes on more debt, her DTI ratio could get too high. She must manage her debts carefully.

Credit: www.militarymoney.com

Frequently Asked Questions

What Is A Debt-to-income Ratio?

The Debt-To-Income Ratio (DTI) measures your debt payments compared to your income.

Why Is Dti Important For Loan Eligibility?

Lenders use DTI to assess your ability to repay loans. Lower DTI means lower risk.

How Do You Calculate Dti?

Divide your total monthly debt payments by your gross monthly income. Multiply by 100 for percentage.

What Is A Good Dti Ratio?

A good DTI is 36% or lower. This shows you manage your debts well.

Conclusion

Understanding your Debt-To-Income ratio is important. It helps you know if you can get a loan. A low DTI ratio is good. It means you have less debt and can handle more. If your DTI ratio is high, you can work to lower it. Pay off debts, increase income, and avoid new debt. These steps will help you be a better loan candidate. Remember, banks want to see that you can handle your debts. A good DTI ratio shows them you can.

Keep track of your DTI ratio. It will help you make smart financial choices. And it will help you get the loans you need. Good luck!