Many people need money for different reasons. A personal loan can help. It is a way to borrow money. You can use it for many things. This article explains how a personal loan works.

Credit: www.sofi.com

What is a Personal Loan?

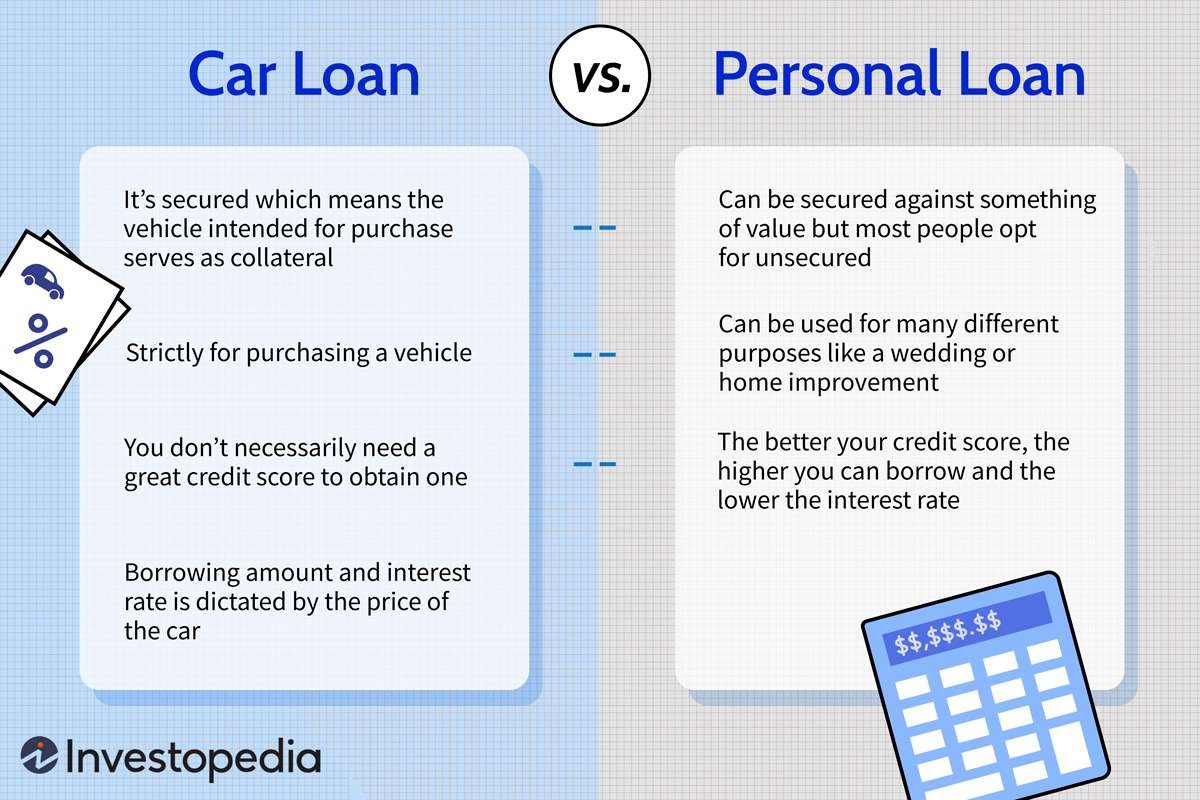

A personal loan is money you borrow from a bank or lender. You must pay it back over time. You also pay interest. Interest is the cost of borrowing money. The bank or lender charges this fee. The loan is not backed by anything you own. This is called an unsecured loan.

Why Do People Get Personal Loans?

People get personal loans for many reasons. Here are some common uses:

- Paying off credit cards

- Home repairs

- Medical bills

- Weddings

- Vacations

Personal loans can help with big expenses. They can also help when you need money fast.

How to Get a Personal Loan

Getting a personal loan is a process. Here are the steps:

1. Check Your Credit Score

Your credit score is important. It shows how well you pay back money. Banks and lenders look at this score. A high score means you are good at paying back money. A low score means you may not pay back money well. Check your score before you apply.

2. Compare Lenders

Not all lenders are the same. Compare different lenders. Look at their interest rates. Look at their terms. Some may have better deals than others. Choose the best one for you.

3. Apply For The Loan

Once you choose a lender, you apply for the loan. You fill out an application. You give personal information. This includes your name, address, and income. The lender checks your credit score. They decide if they will give you the loan.

4. Get The Loan

If you are approved, you get the money. The lender gives you the loan amount. You can use the money for your needs. But remember, you must pay it back.

:max_bytes(150000):strip_icc()/Personal-loans-111715-final-3c39d6d214e44604bdc1efca2525d37d.png)

Credit: www.investopedia.com

Repaying the Loan

Repaying a personal loan is important. Here is how it works:

1. Monthly Payments

You make monthly payments to the lender. Each payment includes principal and interest. The principal is the original amount you borrowed. Interest is the cost of borrowing the money.

2. Fixed Term

Personal loans have a fixed term. This means you have a set amount of time to pay back the loan. Common terms are 2, 3, or 5 years. The term is set when you take out the loan.

3. Fixed Payments

Payments are usually the same each month. This makes it easier to budget. You know how much you need to pay each month.

Benefits of Personal Loans

Personal loans have many benefits. Here are some:

- No collateral needed

- Fixed interest rates

- Fixed monthly payments

- Flexible use of funds

These benefits make personal loans a good option for many people.

Things to Consider

Before getting a personal loan, consider these things:

1. Interest Rates

Interest rates can be high. Make sure you can afford the payments. Compare rates from different lenders.

2. Fees

Some lenders charge fees. These can include application fees, origination fees, or prepayment penalties. Ask about any fees before you apply.

3. Your Budget

Make sure you can fit the loan payments into your budget. Missing payments can hurt your credit score. It can also lead to more fees.

Frequently Asked Questions

What Is A Personal Loan?

A personal loan is money borrowed from a bank or lender.

How Do You Qualify For A Personal Loan?

You need good credit, steady income, and low debt.

What Can You Use A Personal Loan For?

You can use it for debt consolidation, emergencies, or large purchases.

What Is The Interest Rate On Personal Loans?

The interest rate depends on your credit score and lender.

Conclusion

A personal loan can help you get the money you need. It is important to understand how they work. Check your credit score. Compare lenders. Understand the terms. Make sure you can afford the payments. A personal loan can be a good choice if you need money for big expenses. But always borrow responsibly.