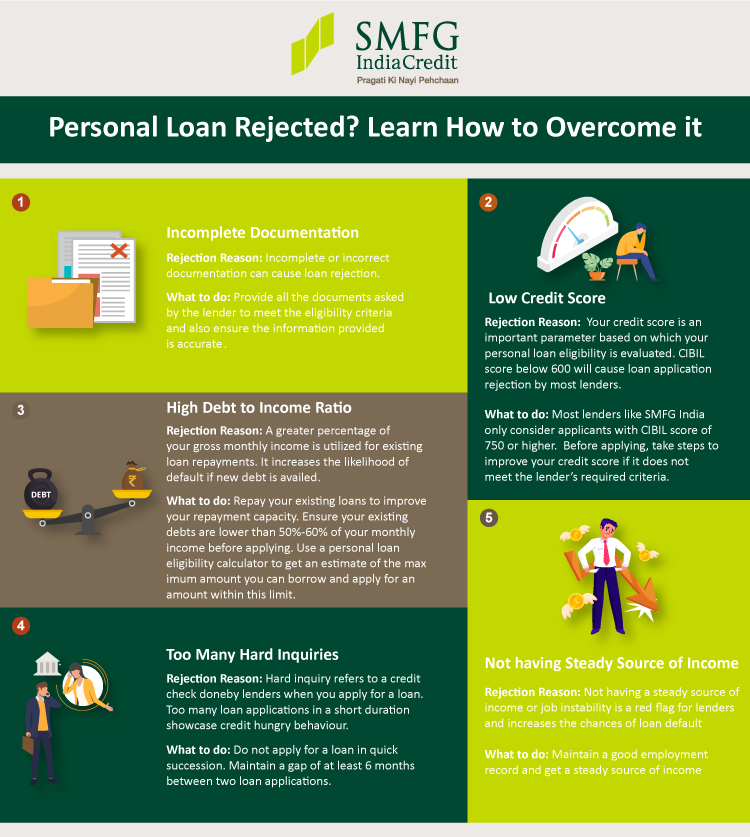

Applying for a personal loan can be stressful. You fill out forms, submit documents, and wait. Sometimes, the answer is “No.” Why do lenders reject personal loan applications? Let’s find out.

Low Credit Score

A low credit score is a common reason. Lenders use credit scores to judge risk. Scores range from 300 to 850. Higher scores mean lower risk. If your score is below 600, you may face rejection.

Improve your score by paying bills on time. Reduce debt. Check your credit report for mistakes. Fix any errors you find.

Credit: www.onescore.app

High Debt-to-Income Ratio

Debt-to-income (DTI) ratio is important. It shows how much of your income goes to debt payments. Lenders prefer a low DTI ratio. A high DTI ratio means you may struggle to repay the loan.

To lower your DTI, pay off some debts. Increase your income if possible. This can improve your chances.

Unstable Employment History

Lenders like stable jobs. They want to see steady income. If you change jobs often, this can be a red flag. Self-employed people may also face challenges.

Show that you have a stable job. Provide proof of income. This can help your application.

Insufficient Income

Lenders need to know you can make payments. If your income is too low, they may reject your application. They want to see that you can afford the loan.

Provide proof of all income sources. Include any side jobs or freelance work. This can strengthen your application.

Incomplete or Inaccurate Application

Filling out the application correctly is crucial. Missing information or mistakes can lead to rejection. Double-check your application before you submit it.

Make sure all information is accurate. Provide all required documents. This shows you are serious and detail-oriented.

:max_bytes(150000):strip_icc()/are-personal-loans-bad-your-credit-score.asp_FINAL-44664c5b7c6b4d73b8ddc4699d545722.png)

Credit: www.investopedia.com

Too Many Recent Loan Applications

Applying for many loans in a short time can hurt your chances. Lenders may see this as a sign of financial trouble.

Space out your loan applications. Avoid applying for multiple loans at once. This can improve your chances of approval.

Existing Financial Commitments

If you have many existing loans, lenders may hesitate. They may worry you can’t handle more debt.

Pay off some of your current loans. Reduce your financial commitments. This can make you a more attractive borrower.

Loan Purpose

Sometimes, the reason for the loan matters. Lenders may be cautious if the loan purpose seems risky.

Be clear and honest about why you need the loan. Provide details if necessary. This can help your case.

Age of Credit History

A short credit history can be a problem. Lenders prefer borrowers with longer credit histories.

Build your credit history over time. Use credit responsibly. This can improve your chances in the future.

Bankruptcy or Foreclosure

Past bankruptcy or foreclosure can hurt your application. Lenders see these as signs of financial instability.

Rebuild your credit after such events. Show that you are now financially responsible. This can help you get approved.

Frequently Asked Questions

Why Do Lenders Reject Personal Loans?

Lenders reject personal loans due to low credit scores, high debt-to-income ratios, or incomplete applications.

How Does Credit Score Affect Loan Approval?

Credit scores show your financial reliability. Low scores suggest risk, leading to rejection.

Can High Debt-to-income Ratio Cause Rejection?

Yes, high debt-to-income ratios indicate you may struggle to repay another loan.

Does Employment History Impact Personal Loan Approval?

Yes, unstable employment history can lead to rejection. Lenders prefer steady income.

Conclusion

Lenders reject personal loan applications for many reasons. Low credit scores, high DTI ratios, and unstable jobs are common factors. Insufficient income and incomplete applications also play a role.

By understanding these reasons, you can improve your chances. Take steps to build your credit, reduce debt, and provide accurate information. This can help you get the loan you need.