Getting a loan is a big decision. You need to know the total cost. This guide will help you understand how to estimate total loan costs. Follow these simple steps and be informed.

Credit: resourcecenter.byupathway.org

Understanding Loan Basics

First, let’s talk about the basics. A loan is money you borrow. You have to pay it back with interest. Interest is a fee for borrowing money. The total loan cost includes the amount borrowed and the interest.

Key Factors In Loan Costs

Several factors affect loan costs. These include:

- Loan Amount

- Interest Rate

- Loan Term

- Fees

Credit: www.wallstreetmojo.com

Step 1: Know Your Loan Amount

The loan amount is the money you borrow. It is also called the principal. This is the starting point for calculating total costs. For example, if you borrow $10,000, your loan amount is $10,000.

Step 2: Understand Interest Rates

Interest rates are very important. They determine how much extra you pay. The rate is usually shown as a percentage. For example, a 5% interest rate means you pay 5% of the loan amount each year.

There are two types of interest rates:

- Fixed Rate: The rate stays the same for the whole loan term.

- Variable Rate: The rate can change over time.

Step 3: Consider the Loan Term

The loan term is the time you have to pay back the loan. It can be short-term or long-term. A short-term loan might be 1-5 years. A long-term loan might be 10-30 years.

Longer terms mean lower monthly payments. But, you pay more in interest over time. Shorter terms mean higher monthly payments. But, you pay less in interest overall.

Step 4: Calculate Monthly Payments

Monthly payments are the amount you pay each month. This includes part of the principal and part of the interest. Use a loan calculator to find your monthly payments. Many websites have free loan calculators.

Step 5: Add Up the Fees

Loans often have extra fees. These can include:

- Origination Fees

- Processing Fees

- Late Payment Fees

Check your loan agreement for all fees. Add these fees to your total loan cost.

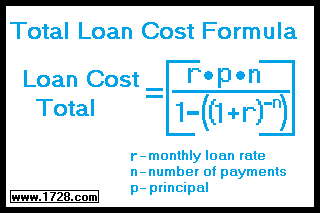

Step 6: Calculate the Total Loan Cost

Now, let’s put it all together. Follow these steps:

- Find your loan amount (principal).

- Determine your interest rate.

- Calculate your monthly payments using a loan calculator.

- Multiply the monthly payment by the number of months in the loan term.

- Add any extra fees.

This will give you the total loan cost.

Example Calculation

Let’s look at an example:

Imagine you borrow $10,000 at a 5% interest rate for 5 years. Your monthly payment might be around $188.71. Multiply this by 60 months (5 years). This equals $11,322.60. If you have $200 in fees, add this to the total. Your total loan cost is $11,522.60.

Importance of Estimating Loan Costs

Knowing the total loan cost helps you plan. It shows you what you can afford. It helps you compare different loans. This way, you can choose the best option.

Tips for Managing Loan Costs

Here are some tips to manage loan costs:

- Shop around for the best interest rates.

- Consider shorter loan terms to save on interest.

- Pay more than the minimum monthly payment.

- Avoid late payments to prevent extra fees.

Frequently Asked Questions

What Are Total Loan Costs?

Total loan costs include principal, interest, fees, and insurance.

How To Calculate Loan Interest?

Multiply the principal by the interest rate and the loan term.

What Is A Loan Principal?

The principal is the original amount borrowed.

Are There Hidden Loan Fees?

Yes, some loans have hidden fees like origination fees or processing charges.

Conclusion

Estimating total loan costs is easy. Know your loan amount, interest rate, and term. Calculate your monthly payments and add any fees. This helps you make smart financial decisions. Now, you are ready to estimate your loan costs.