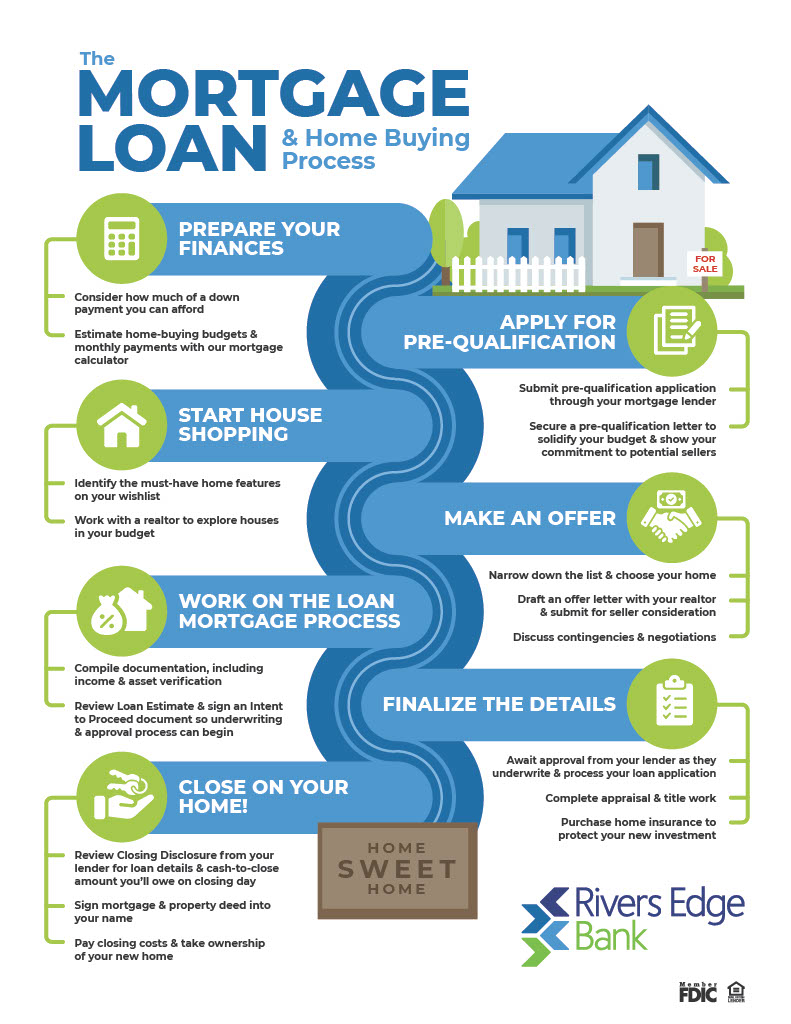

Getting a loan approved is a big step. But what happens next? Let’s break it down.

Welcome Letter

After your loan is approved, you will receive a welcome letter. This letter gives you important information about your loan. It includes the loan amount, interest rate, and repayment schedule.

Loan Agreement

Next, you will need to sign a loan agreement. This is a contract between you and the lender. It explains the terms and conditions of the loan. Read it carefully before signing.

Disbursement of Funds

After signing the loan agreement, the funds will be disbursed. This means the money will be sent to you or used to pay off other loans. The disbursement process can take a few days.

Loan Repayment

Once the funds are disbursed, you will start repaying the loan. The repayment schedule is usually monthly. Make sure to pay on time to avoid late fees.

Types Of Repayment Plans

- Fixed-Rate Loans: The interest rate stays the same. Your monthly payment is the same each month.

- Variable-Rate Loans: The interest rate can change. Your monthly payment can go up or down.

Credit: www.rate.com

Interest Rates

The interest rate is the cost of borrowing money. It is a percentage of the loan amount. Fixed-rate loans have the same interest rate for the life of the loan. Variable-rate loans can have changing interest rates.

Keeping Track of Payments

It is important to keep track of your loan payments. You can use a calendar or set reminders. Many lenders offer online tools to help you manage your loan.

Setting Up Automatic Payments

Consider setting up automatic payments. This ensures your payments are made on time. It can also help you avoid late fees.

Credit: riversedge.bank

Loan Statements

You will receive loan statements. These statements show your payment history. They also show the remaining balance on your loan.

Customer Service

If you have questions, contact customer service. They can help you understand your loan and payments. Most lenders offer phone and email support.

Refinancing Options

In the future, you may want to refinance your loan. Refinancing means getting a new loan to pay off the old one. This can help you get a lower interest rate or better terms.

Impact on Credit Score

Repaying your loan on time can improve your credit score. A higher credit score can help you get better loan terms in the future. Late payments can hurt your credit score.

What if You Can’t Pay?

If you can’t make a payment, contact your lender right away. They may offer options to help you. These options can include deferment or forbearance. Deferment allows you to stop making payments for a short time. Forbearance reduces your payments for a short time.

Frequently Asked Questions

What Should I Do After Loan Approval?

Review and sign the loan agreement. Follow lender instructions.

How Long Does It Take To Get Funds?

Usually, it takes a few days. Check with your lender.

Can My Loan Be Canceled After Approval?

Yes, if you don’t meet conditions. Stay in touch with your lender.

What Documents Are Needed Post-loan Approval?

Typically, ID proof, income proof, and signed agreement.

Conclusion

Understanding what happens after loan approval is important. This helps you stay on top of your payments. It also ensures you don’t miss any important steps. Follow these guidelines to manage your loan successfully.