Loans are helpful in many situations. You might need money for a car, house, or school. But what if you need more than one loan? Can you apply for multiple loans at once? Let’s find out.

Why People Apply for Loans

People apply for loans for different reasons. Some common reasons include:

- Buying a house

- Buying a car

- Paying for school

- Starting a business

- Consolidating debt

Loans can help you achieve your goals. But applying for multiple loans at once can be tricky.

What Happens When You Apply for Multiple Loans?

Applying for multiple loans at once can have effects. These effects can be good or bad. Let’s look at the details.

Impact On Credit Score

When you apply for a loan, the lender checks your credit score. This is called a “hard inquiry.” Too many hard inquiries can lower your credit score. This is because lenders see you as a risk.

Better Chances Of Approval

Applying for multiple loans can increase your chances of approval. If one lender says no, another might say yes. But remember, each application affects your credit score.

More Choices

When you apply for multiple loans, you have more choices. You can compare interest rates and terms. This helps you find the best deal. But be careful. Too many applications can hurt your credit score.

Credit: www.idfcfirstbank.com

Types of Loans You Can Apply For

There are many types of loans. Here are some common ones:

- Personal Loans: These loans can be used for many things. You can use them for home repairs, medical bills, or vacations.

- Auto Loans: These loans are for buying a car. They have fixed interest rates and terms.

- Home Loans: These loans are for buying a house. They can be long-term loans, like 15 or 30 years.

- Student Loans: These loans are for paying for school. They have lower interest rates and can be deferred until after graduation.

- Business Loans: These loans are for starting or growing a business. They can be short-term or long-term loans.

Each type of loan has its own rules. Make sure you understand them before you apply.

Pros and Cons of Applying for Multiple Loans

Applying for multiple loans has its pros and cons. Let’s look at both.

Pros

- More Options: You have more choices. You can compare interest rates and terms.

- Better Chances: If one lender says no, another might say yes.

- Flexibility: Different loans can be used for different needs.

Cons

- Credit Score Impact: Each application affects your credit score.

- Confusion: Managing multiple loans can be confusing. You need to keep track of payments and terms.

- Debt Risk: More loans mean more debt. This can be risky if you can’t pay them back.

How to Manage Multiple Loan Applications

Applying for multiple loans can be tricky. Here are some tips to help you manage them:

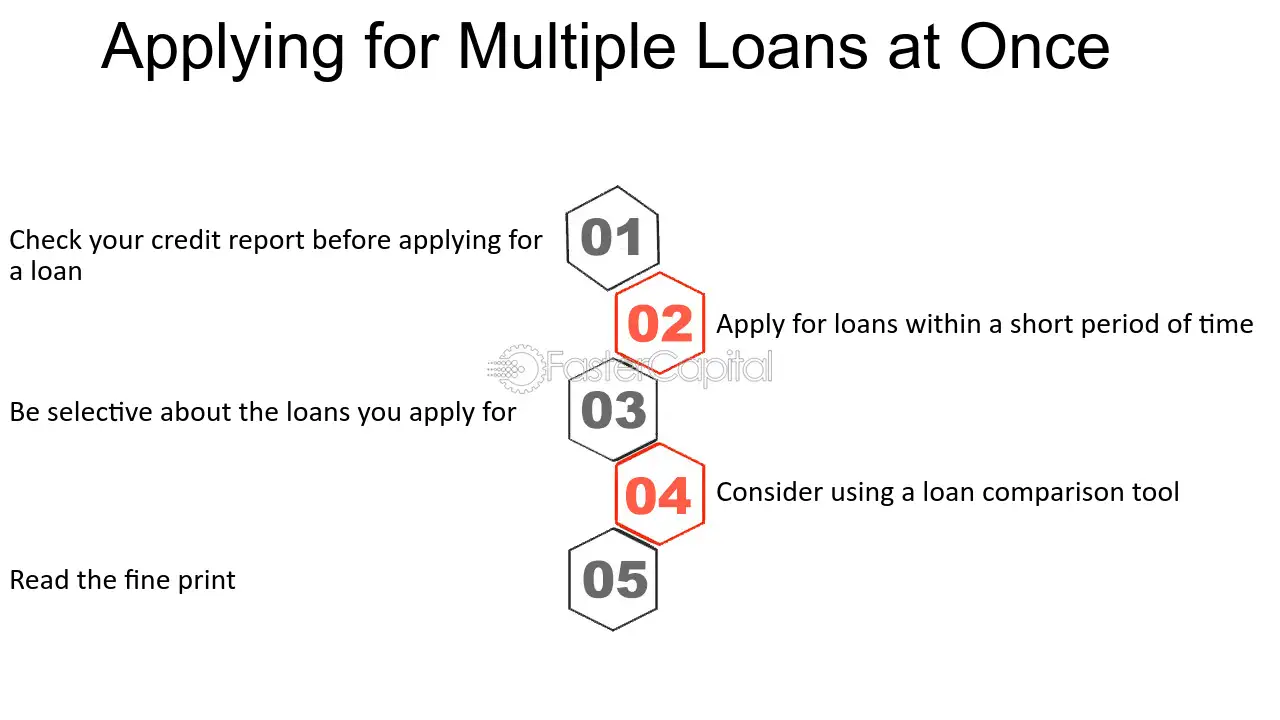

Check Your Credit Score

Before applying for any loan, check your credit score. This helps you understand your chances of approval. It also helps you find loans with better interest rates.

Space Out Your Applications

Don’t apply for all the loans at once. Space out your applications over a few months. This helps reduce the impact on your credit score.

Compare Lenders

Not all lenders are the same. Compare interest rates, terms, and fees. This helps you find the best deal.

Read The Terms

Before accepting any loan, read the terms carefully. Make sure you understand the interest rate, payment schedule, and fees.

Keep Track Of Payments

If you have multiple loans, keep track of your payments. Use a calendar or an app to remind you. Missing payments can hurt your credit score.

Credit: www.loantube.com

When Applying for Multiple Loans Makes Sense

There are times when applying for multiple loans makes sense. Here are some examples:

Debt Consolidation

If you have many small debts, you can use a loan to pay them off. This is called debt consolidation. It helps you manage your payments better.

Large Expenses

If you have a big expense, like a home repair, you might need more than one loan. This helps you cover the cost.

Business Growth

If you are growing your business, you might need multiple loans. This helps you buy equipment, hire staff, or expand your office.

Frequently Asked Questions

Can You Apply For Multiple Loans At Once?

Yes, you can apply for multiple loans. But it’s not always a good idea.

Does Applying For Multiple Loans Affect Credit Score?

Yes, multiple loan applications can lower your credit score. Each application is a hard inquiry.

How Many Loans Can I Apply For At One Time?

There is no set limit. But too many applications can hurt your credit score.

Should I Apply For Multiple Loans Together?

It’s best to avoid applying for many loans at once. It can harm your credit score.

Conclusion

Can you apply for multiple loans at once? Yes, you can. But it has pros and cons. It can affect your credit score and add to your debt. Make sure you understand the risks. Compare lenders, read the terms, and keep track of your payments. This helps you manage your loans better.

If you need more help, talk to a financial advisor. They can give you advice based on your situation.