Your Debt-To-Income (DTI) ratio is important. It helps lenders decide if you can pay back a loan. This article will explain what the DTI ratio is. We will see how it affects loan approval.

What is Debt-To-Income Ratio?

The Debt-To-Income ratio is a number. It shows how much of your income goes to paying debts. This includes loans, credit cards, and other payments. Lenders look at this number closely.

How To Calculate Your Dti Ratio

Calculating your DTI ratio is simple. Here are the steps:

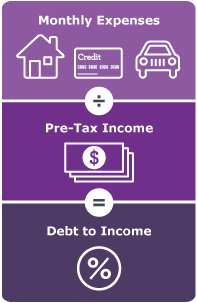

- Add up all your monthly debt payments.

- Include mortgage, car loans, credit cards, and other debts.

- Divide this total by your gross monthly income.

- Multiply the result by 100 to get a percentage.

Here is the formula:

DTI Ratio = (Total Monthly Debt Payments / Gross Monthly Income) x 100

Example Calculation

Let’s say you have the following monthly debts:

- Mortgage: $1,200

- Car Loan: $300

- Credit Cards: $200

- Student Loans: $250

Your total monthly debt payments would be:

$1,200 + $300 + $200 + $250 = $1,950

If your gross monthly income is $5,000, your DTI ratio is:

Credit: www.wellsfargo.com

Why DTI Ratio is Important for Loan Approval

Lenders use the DTI ratio to see if you can handle more debt. A lower DTI ratio is better. It means you have more money to pay new loans.

Good Dti Ratios For Loan Approval

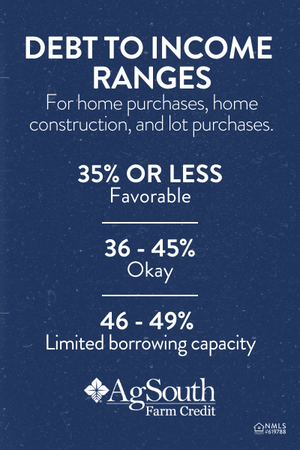

Different lenders have different standards. But here are some general guidelines:

- 36% or less: This is a good DTI ratio. You are likely to get loan approval.

- 37% to 49%: This is an acceptable range. You may still get a loan, but it could be harder.

- 50% or more: This is a high DTI ratio. Lenders may think you have too much debt. It will be hard to get a loan.

Credit: www.agsouthfc.com

How to Improve Your DTI Ratio

If your DTI ratio is high, do not worry. There are ways to improve it. Here are some tips:

Pay Off Debts

Focus on paying off your debts. Start with the smallest debt. Then move on to the next. This is known as the “snowball method.”

Increase Your Income

Another way to lower your DTI ratio is to increase your income. You can take a second job. Or you can work extra hours. Any extra money helps.

Avoid New Debts

Do not take on new debts. This will only make your DTI ratio worse. Wait until your DTI ratio improves before getting new loans.

Frequently Asked Questions

What Is A Debt-to-income Ratio?

Debt-To-Income Ratio (DTI) is the percentage of your income that goes towards paying debts.

How Is Dti Calculated?

DTI is calculated by dividing your monthly debt payments by your gross monthly income.

Why Is Dti Important For Loan Approval?

Lenders use DTI to assess if you can afford to take on more debt.

What Is A Good Dti Ratio?

A good DTI ratio is typically below 36%. Lower ratios are preferred by lenders.

Conclusion

Your Debt-To-Income ratio is key for loan approval. It shows lenders if you can handle new debts. Keep your DTI ratio low. Pay off debts and increase your income. This will help you get the loans you need.