Personal loans and credit cards are two popular ways to borrow money. They help you cover expenses when you do not have enough cash. But which one is better? This article will help you decide.

Credit: www.lendingpoint.com

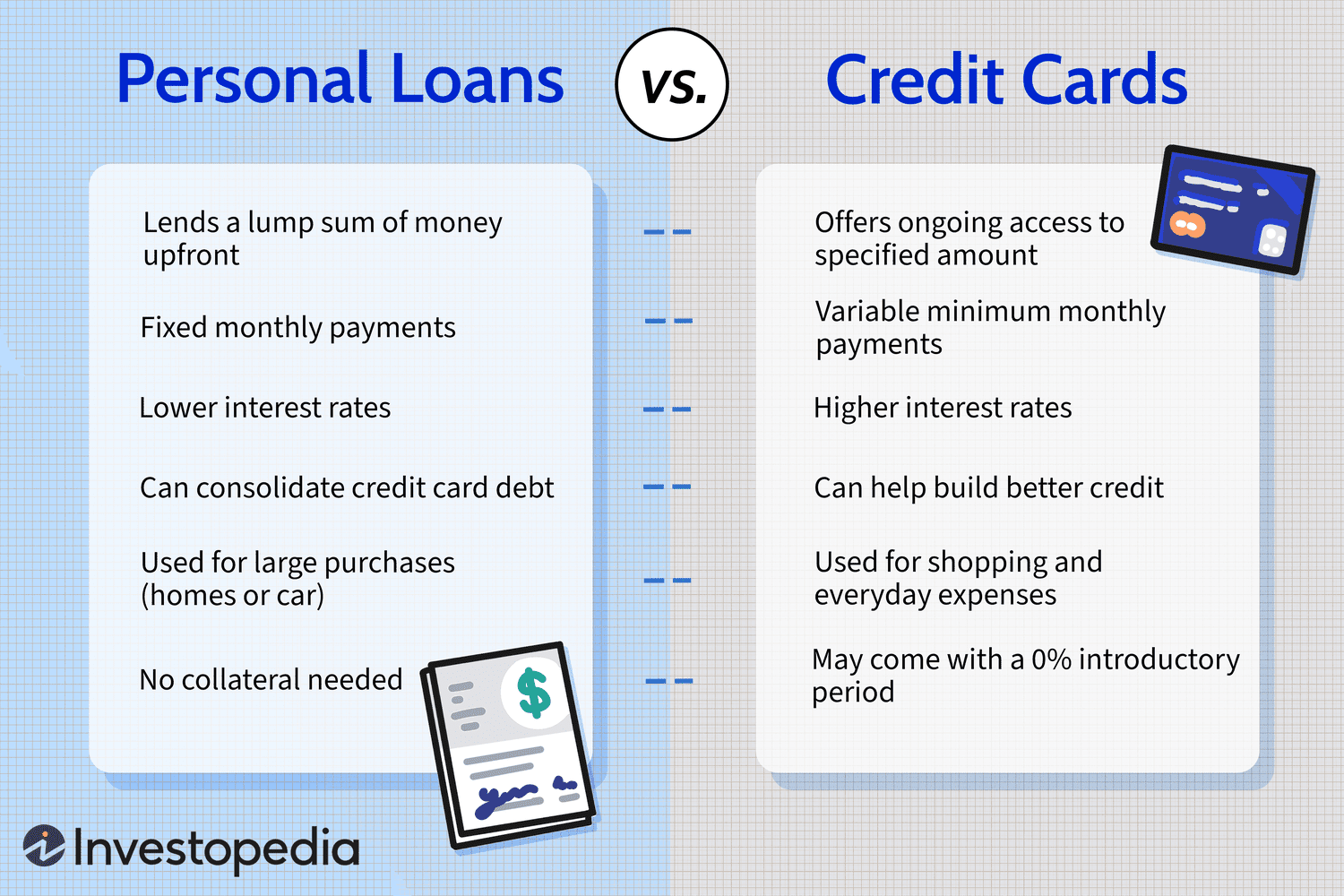

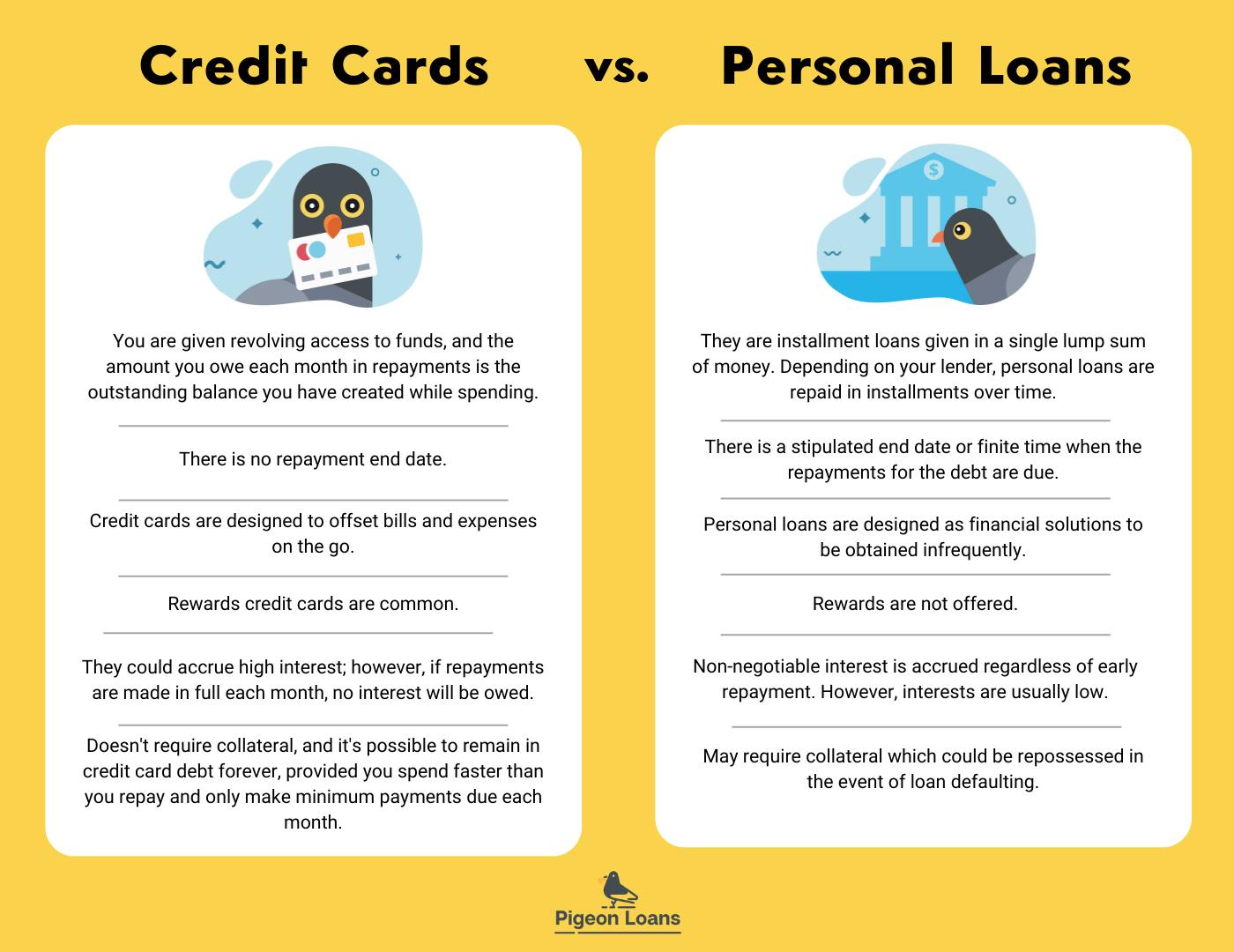

What is a Personal Loan?

A personal loan is money you borrow from a bank or lender. You agree to pay it back over time with interest. Personal loans can be used for many things. You can use them for home repairs, medical bills, or even a vacation.

How Do Personal Loans Work?

You apply for a personal loan with a bank or lender. They check your credit score and income. If they approve you, they give you the money. You then pay back the loan in monthly payments. These payments include interest.

Pros Of Personal Loans

- Fixed monthly payments make budgeting easier.

- Lower interest rates than credit cards.

- You can borrow a large amount of money.

Cons Of Personal Loans

- You need a good credit score to get a low rate.

- There may be fees for applying or paying off early.

- It takes time to get approved and receive the money.

What is a Credit Card?

A credit card is a plastic card issued by a bank. You use it to buy things now and pay later. Credit cards have a credit limit, which is the maximum amount you can borrow.

How Do Credit Cards Work?

You use your credit card to make purchases. Each month, you receive a bill for what you owe. You can pay the full amount or make a minimum payment. If you do not pay the full amount, you will pay interest on the remaining balance.

Pros Of Credit Cards

- Easy and fast to use for everyday purchases.

- Can help build your credit score if used responsibly.

- Many cards offer rewards like cash back or travel points.

Cons Of Credit Cards

- High interest rates if you do not pay the full balance.

- Easy to overspend and get into debt.

- Late payments can hurt your credit score.

Comparing Personal Loans and Credit Cards

Now that you know about personal loans and credit cards, let’s compare them. This will help you decide which one is better for you.

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Interest Rate | Usually lower | Usually higher |

| Repayment | Fixed monthly payments | Flexible, but minimum payment required |

| Fees | May have application or early payoff fees | May have annual fees or late payment fees |

| Credit Score Impact | Can improve score if paid on time | Can improve score if used responsibly |

| Approval Time | Takes longer | Faster |

| Best For | Large expenses | Everyday purchases |

When to Choose a Personal Loan

Choose a personal loan if you need a large amount of money. It is also good if you want fixed monthly payments. This makes it easier to budget. Personal loans are best for planned expenses. For example, home renovations or debt consolidation.

Examples Of Good Uses For Personal Loans

- Home improvement projects

- Medical bills

- Debt consolidation

- Major life events like weddings

When to Choose a Credit Card

Choose a credit card for everyday purchases. It is also good for small expenses that you can pay off quickly. Credit cards are best if you can pay the full balance each month. This way, you avoid interest charges. They are also good for building your credit score.

Examples Of Good Uses For Credit Cards

- Groceries and gas

- Online shopping

- Travel and dining

- Emergency expenses

Frequently Asked Questions

What Are The Main Differences Between Personal Loans And Credit Cards?

Personal loans offer lump-sum money. Credit cards offer revolving credit. Both have different interest rates and terms.

Which Is Better For Large Expenses: Personal Loans Or Credit Cards?

Personal loans are usually better for large expenses due to lower interest rates and fixed payments.

How Do Interest Rates Compare Between Personal Loans And Credit Cards?

Personal loans often have lower interest rates than credit cards, which usually have higher variable rates.

Can I Use Personal Loans For Debt Consolidation?

Yes, personal loans can consolidate high-interest debts into one lower-interest payment. It simplifies and saves money.

Conclusion

Personal loans and credit cards both have their benefits. Personal loans are better for large, planned expenses. They offer lower interest rates and fixed payments. Credit cards are better for everyday purchases and smaller expenses. They offer convenience and rewards. Choose the option that fits your financial needs best. Remember to use both responsibly to maintain good credit.