Applying for a loan is a big step. It can help you buy a house, start a business, or pay for school. But many people make mistakes when they apply for loans. These mistakes can cause delays or even lead to rejection. Let’s talk about some of the most common mistakes in loan applications.

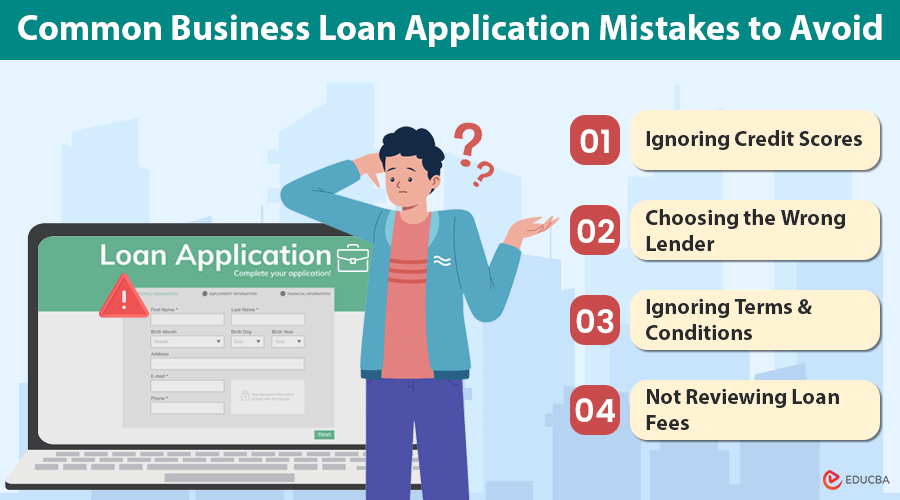

1. Not Checking Credit Score

Your credit score is very important. It shows how good you are at paying back money. If your credit score is low, banks might not want to give you a loan. Before you apply for a loan, check your credit score. Make sure it is good enough.

2. Providing Incorrect Information

Always be honest on your loan application. Provide the correct information about your income, job, and expenses. If you give wrong details, the bank might reject your application. Double-check all the information before you send it.

3. Applying for Too Many Loans

Do not apply for many loans at the same time. Each application affects your credit score. If you apply for too many loans, it can lower your score. This makes it harder to get a loan.

4. Ignoring Loan Terms and Conditions

Always read the terms and conditions of the loan. They tell you about the interest rate, monthly payments, and other fees. If you do not understand something, ask the bank to explain. Do not ignore these details.

5. Missing Documents

When you apply for a loan, you need to provide some documents. These might include your ID, proof of income, and bank statements. Make sure you have all the required documents. Missing documents can delay your application.

6. Not Having a Stable Job

Banks like to see that you have a stable job. It shows that you can pay back the loan. If you change jobs often, it might be harder to get a loan. Try to stay in one job for a while before you apply for a loan.

7. Borrowing More Than You Can Pay

Only borrow what you can afford to pay back. Calculate your monthly income and expenses. Make sure you can make the loan payments. If the payments are too high, you might get into trouble.

Credit: www.youtube.com

8. Not Comparing Different Loans

There are many types of loans. Each one has different terms and interest rates. Compare different loans to find the best one for you. Do not just choose the first loan you see.

9. Not Having a Plan

Have a clear plan for how you will use the loan. Banks want to see that you have a good reason for borrowing money. Explain your plan clearly in your application.

Credit: money911.ca

10. Ignoring Your Debt-to-Income Ratio

The debt-to-income ratio is important. It shows how much of your income goes to pay debts. If this ratio is too high, banks might not give you a loan. Try to lower your debts before you apply for a loan.

Summary

Applying for a loan can be easy if you avoid common mistakes. Check your credit score, provide correct information, and have all your documents ready. Make sure you have a stable job and borrow only what you can pay back. Read the loan terms and compare different loans. Have a clear plan for the loan and watch your debt-to-income ratio.

Frequently Asked Questions

What Are The Common Loan Application Mistakes?

Errors on forms, missing documents, and incorrect income details are common mistakes.

How Does Incorrect Income Affect Loan Approval?

Incorrect income details can lead to loan rejection. Always provide accurate income information.

Why Is Credit Score Important For Loans?

A good credit score improves your chances of loan approval and lower interest rates.

Can Missing Documents Delay Loan Approval?

Yes, missing documents can delay or even stop the loan approval process.

Conclusion

By avoiding these common mistakes, you can improve your chances of getting a loan. Take your time with the application. Make sure everything is correct and complete. Good luck with your loan application!