Business loans help companies grow. They provide needed funds. But getting a loan can be tough. One important factor is collateral. Let’s explore what collateral is and why it matters.

What is Collateral?

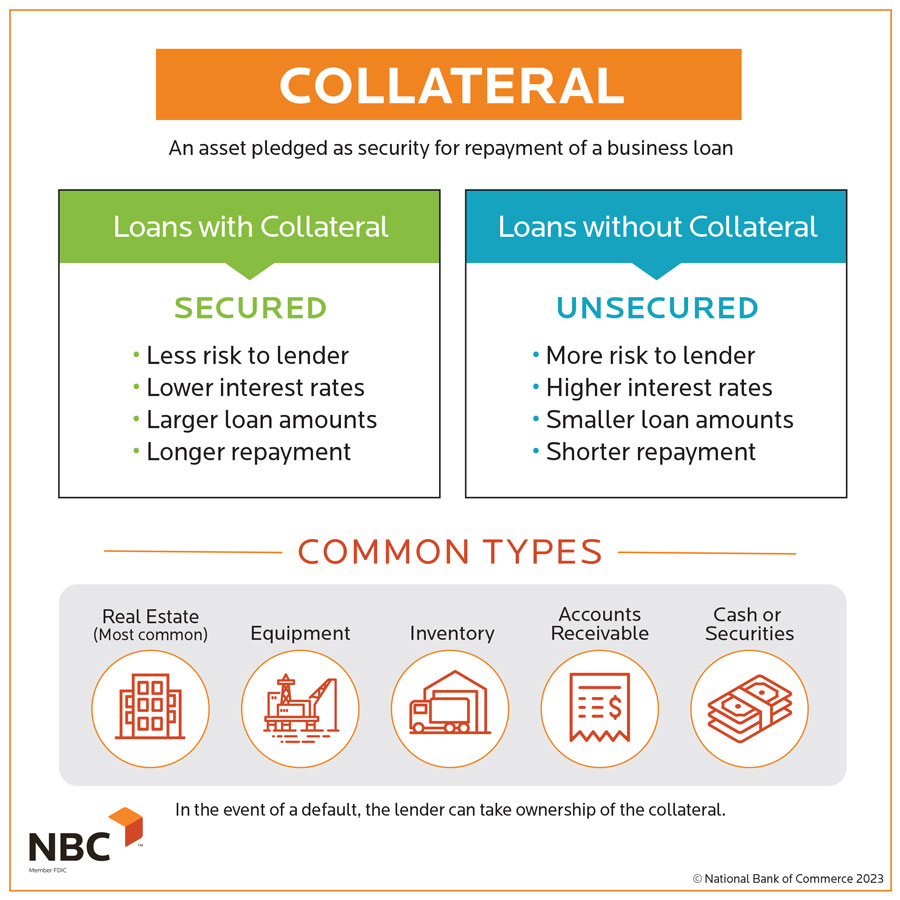

Collateral is something of value. It is given to secure a loan. If the borrower cannot repay, the lender takes the collateral. This reduces the lender’s risk.

Why is Collateral Important?

Collateral makes lenders feel safe. They know they can recover their money. This is important because lending money is risky. Some businesses fail. When this happens, lenders may lose their money. Collateral helps reduce this risk.

How Collateral Affects Loan Approval

Collateral plays a big role in loan approval. Lenders look at the value of the collateral. They also consider the type. Strong collateral increases the chances of getting a loan. Weak collateral may lead to denial.

Credit: theenterpriseworld.com

Types of Collateral

There are different types of collateral. Each type has its own value. Let’s look at some common types:

- Real Estate: This includes buildings and land. Real estate is high-value collateral.

- Equipment: This includes machinery and tools. Equipment is useful for manufacturing businesses.

- Inventory: This includes products ready for sale. Inventory can be valuable.

- Accounts Receivable: This includes money owed to the business. It shows that cash is coming.

- Savings: This includes bank accounts. Lenders like cash as collateral.

Real Estate

Real estate is very valuable. It includes buildings and land. Lenders like real estate. It rarely loses value. Business owners can use their office or factory as collateral. This can help secure a large loan.

Equipment

Equipment can also be used as collateral. This includes machines, tools, and vehicles. Equipment is essential for many businesses. Lenders consider its value. They also think about its age. Newer equipment is worth more.

Inventory

Inventory is another type of collateral. This includes products ready for sale. Inventory has value. But it can lose value over time. For example, fashion items may go out of style. Lenders consider this when evaluating inventory.

Accounts Receivable

Accounts receivable can be collateral. This is money owed to the business. It shows that cash is coming. Lenders like this. But they also consider the risk. If customers do not pay, accounts receivable lose value.

Savings

Savings are the simplest form of collateral. This includes money in bank accounts. Lenders like cash. It is easy to value. It also does not lose value. Savings make strong collateral.

How to Use Collateral

Using collateral is a process. First, the borrower offers the collateral. The lender then evaluates it. If the lender approves, they give the loan. If the borrower cannot repay, the lender takes the collateral.

Steps To Use Collateral

- Identify the collateral.

- Offer it to the lender.

- The lender evaluates the collateral.

- The lender approves or denies the loan.

- If approved, the loan is given.

- If the borrower cannot repay, the lender takes the collateral.

Benefits of Using Collateral

Using collateral has many benefits. It can help secure a loan. It can also lead to better loan terms. Let’s explore these benefits.

Higher Loan Amounts

Strong collateral can lead to higher loan amounts. Lenders feel safe lending more money. This can help businesses grow faster.

Better Interest Rates

Collateral can lead to better interest rates. Lenders offer lower rates to reduce risk. This can save businesses money over time.

Longer Repayment Terms

Collateral can lead to longer repayment terms. Lenders feel safe giving more time. This can help businesses manage cash flow.

Improved Loan Approval Chances

Collateral improves loan approval chances. Lenders are more likely to approve loans with strong collateral. This can help businesses secure needed funds.

Credit: www.nbcbanking.com

Risks of Using Collateral

Using collateral has risks. If the borrower cannot repay, they lose the collateral. This can hurt the business. It can also hurt the owner’s personal finances. Let’s look at these risks.

Loss Of Business Assets

If the borrower cannot repay, they lose business assets. This can include buildings, equipment, or inventory. Losing these can hurt the business.

Personal Financial Risk

Some business owners use personal assets as collateral. This can include their home or savings. If the business fails, they lose these assets. This can hurt their personal finances.

Impact On Credit Score

Defaulting on a loan can hurt the borrower’s credit score. This makes it harder to get future loans. It can also lead to higher interest rates.

Frequently Asked Questions

What Is Collateral In Business Loans?

Collateral is an asset pledged to secure a business loan.

Why Do Lenders Require Collateral?

Lenders need collateral to reduce risk and ensure loan repayment.

What Types Of Collateral Can Be Used?

Common collateral includes real estate, equipment, inventory, and accounts receivable.

How Does Collateral Affect Loan Approval?

Strong collateral improves chances of loan approval and better terms.

Conclusion

Collateral plays a key role in business loans. It helps secure loans and reduce risk. There are many types of collateral. Each has its own value. Using collateral has benefits and risks. Business owners must consider these before using collateral. By understanding collateral, businesses can make better loan decisions.